2014 is right around the corner and it’s about that time to highlight

our most downloaded papers from the past year. These articles covered it

all – organ transplants, game theory, asset management, government

surveillance and privacy and beyond.

Congrats and cheers from all of us at SSRN!

Science is a very serious business, so what tickles a rational

mind? In a not very scientific experiment, we asked a sample of great

minds for their favourite jokes

Batman: salt of the earth. Photograph: Allstar/Cinetext/20 CENTURY FOX

Physics

■ Two theoretical physicists are lost at the top of a mountain.

Theoretical physicist No 1 pulls out a map and peruses it for a while.

Then he turns to theoretical physicist No 2 and says: "Hey, I've figured

it out. I know where we are."

"Where are we then?"

"Do you see that mountain over there?"

"Yes."

"Well… THAT'S where we are."

I heard this joke at a physics conference in Les Arcs (I was at the

top of a mountain skiing at the time, so it was quite apt). It was

explained to me that it was first told by a Nobel prize-winning

experimental physicist by way of indicating how out-of-touch with the

real world theoretical physicists can sometimes be. Jeff Forshaw, professor of physics and astronomy, University of Manchester

■ An electron and a positron go into a bar.

Positron: "You're round."

Electron: "Are you sure?"

Positron: "I'm positive."

I

think I heard this on Radio 4 after the publication of a record (small)

measurement of the electron electric dipole moment – often explained as

the roundness of the electron – by Jony Hudson et al in Nature 2011. Joanna Haigh, professor of atmospheric physics, Imperial College, London

■ A group of wealthy investors wanted to be able to predict the

outcome of a horse race. So they hired a group of biologists, a group of

statisticians, and a group of physicists. Each group was given a year

to research the issue. After one year, the groups all reported to the

investors. The biologists said that they could genetically engineer an

unbeatable racehorse, but it would take 200 years and $100bn. The

statisticians reported next. They said that they could predict the

outcome of any race, at a cost of $100m per race, and they would only be

right 10% of the time. Finally, the physicists reported that they could

also predict the outcome of any race, and that their process was cheap

and simple. The investors listened eagerly to this proposal. The head

physicist reported, "We have made several simplifying assumptions:

first, let each horse be a perfect rolling sphere… "

This is really the joke form of "all models are wrong, some models

are useful" and also sums up the sort of physics confidence that they

can solve problems (ie, by making the model solvable). Ewan Birney, associate director, European Bioinformatics Institute

■ What is a physicist's favourite food? Fission chips. Callum Roberts, professor in marine conservation, University of York

This is real short term stuff.

Contrary indicator: Gold reversed this morning's declines and is now up on the day by a few cents.

We've mentioned before that First Solar (FSLR) has shown some predictive ability, with anywhere from a 1 day to 1 week lag.

After being a major gainer during 2013 it is down 2% today.

Ditto for another of the more speculative issues, Tesla. Biggest gainer among major stocks in 2013, down 2.26% today.

S&P 500 Index 1846.36 up 5.29

DJIA 16,552.43 up 48.14.

TSLA $149.00

FSLR $54.51

For all the endless talk of a recovery during the past five years,

there is a very tangible reason why for most people this is nothing but

spin, propaganda and lies: when one strips away the retroactively

adjusted GDP, the seasonally adjusted (and politically mandated)

counting of temp jobs, the constantly upward revised jobless claims, the

Fed's $4+ trillion balance sheet of course, and even the declining (yes, declining) real disposable income per capita, what

one is left with is the lowest loan creation out of a recession (or

depression) in history, and is at indexed levels last seen during the

Lehman collapse over five years ago!

Why is loan creation important? Because in traditional economics (not

their "New Normal" equivalent, where central planning decides

everything), loans - i.e., money created by commercial banks -

ultimately leads to GDP growth. It also has a direct bearing on the

steepness of the bond curve and thus, inflation expectations.

Conversely, lack of loan creation ultimately means the

government is forced to adjusted the definition of GDP to make it seem

as if there is growth, or to rely on an inventory stockpiling boost to

"growth" and all other recently seen gimmicks to force the conviction of

"growth."

There's more. As the charts below show, there is a direct link

between loan demand (and thus creation), and EPS growth, Industrial

Production, Employment and CRE development. Obviously, the lower the

loan creation, the worse all of these will look.

But how is it possible that banks continue to function in an

environment in which there has been zero loan creation for the past 5

years? Simple: the banks' excess deposits (a liability) has been pumped

higher by about $2.5 trillion thanks to the Fed's excess deposits...MORE

From anti-austerity movements to middle-class revolts, in

rich countries and in poor, social unrest has been on the rise around

the world. The reasons for the protests vary. Some are direct responses

to economic distress (in Greece and Spain, for example). Others are

revolts against dictatorship (especially in the Middle East). A number

also express the aspirations of new middle classes in fast-growing

emerging markets (whether in Turkey or Brazil). But they share some

underlying features.

The common backdrop is the 2008-09 financial crisis and its

aftermath. Economic distress is almost a necessary condition for serious

social or political instability, but it is not a sufficient one.

Declines in income and high unemployment are not always followed by

unrest. Only when economic trouble is accompanied by other elements of

vulnerability is there a high risk of instability. Such factors include

wide income-inequality, poor government, low levels of social provision,

ethnic tensions and a history of unrest. Of particular importance in

sparking unrest in recent times appears to have been an erosion of trust

in governments and institutions: a crisis of democracy.

Trust has been in secular decline

throughout the rich world since the 1970s. This trend accelerated and

spread after the collapse of communism in 1989. And as opinion polls

have documented, it has sped up again since the 2008–09 financial

crisis.

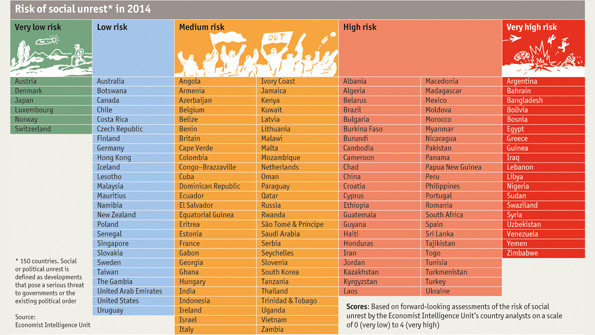

65 countries will be at a high or very high risk

The Economist Intelligence Unit (EIU), a sister company of The Economist,

measures the risk of social unrest in 150 countries around the world.

It places a heavy emphasis on institutional and political weaknesses.

And recent developments have indeed revealed a deep sense of popular

dissatisfaction with political elites and institutions in many emerging

markets.

The protesters in Turkey in 2013, for example, were

dissatisfied with some abrupt decisions by Recep Tayyip Erdogan’s

government. In Bulgaria, what started off as protests against higher

electricity bills turned into generalised anti-government demonstrations

complaining of corruption—and led to the fall of the government.

Protests have continued.

What to expect in 2014? The recession is now over or has

eased in much of the world. Yet political reactions to economic distress

have historically come with a lag. Austerity is still on the agenda in

2014 in many countries and this will fuel social unrest....MORE

From Reuters via agProfessional: High cash rents to squeeze Midwest grain farmers in 2014

Rents on prime U.S. crop land are expected to stay high in 2014

despite a sharp drop in grain prices, raising financial pressure on

farmers who rent most of their land and risk big losses in the coming

year, analysts and bankers say.

More than half the 250 million acres (101 million hectares) of corn,

soybean and wheat land in the United States, the world's biggest grain

exporter, are rented. Negotiations on 2014 farm land leases are going on

in the Corn Belt and Great Plains, with farmers, absentee owners and

their farm managers, and farm lenders all penciling out projected grain

growing profits and losses.

"With the recent drop in crop prices and the stickiness of land rents

not falling as quickly as crop prices, many farmers are feeling the

squeeze once again between revenue, costs and rent," said Kent Olson, an

economist at the University of Minnesota.

That is a marked difference from five years of record or near-record

farm income driven by record demand for biofuels and exports, capped

with record grain prices in 2012 during the worst U.S. drought in 50

years. Now things have changed. The record large U.S. harvest in 2013

bins has dropped grain prices 30 percent in six months.

Bottom-line estimates for growing corn in 2013 in northern Illinois,

for instance, now project a loss of $81 an acre compared to net gains of

$188 an acre in 2012 and $251 in 2011, according to farm economist Gary

Schnitkey of the University of Illinois.

For 2014, projections based on current costs and prices pencil out to

a loss of $53 an acre for corn, he says. The outlook is similar in Iowa

and Minnesota, which with Illinois produce more than a third of all

U.S. corn and soybeans.

The problem for renters, though, is two-fold. Lease rates almost

always lag drops in grain prices as landowners see what the market will

bear. And farmers usually chase land prices for fear of losing the

acreage in future to some other neighbor who will risk and pay more....MORE

As with most commodities, the copper market was driven by China in

2013 and there is every reason to believe the Asian giant will remain in

the driver's seat in 2014.

But, while China remains the driver, 2014 could well mark the year

the metal switches from the demand car to the supply car as Chinese

consumption levels peak and new sources of supply come on stream.

According to Wood MacKenzie's Sophie Chung, total copper consumption

is expected to grow at around 4% per annum over the next five years,

with China being the main user.

Speaking at Mines and Money in London earlier this month, Chung

explained that, while Chinese demand is expected to remain robust over

the coming years, "based on how China has grown since 2000, we expect

its peak consumption rate to peak in 2013, just below the peak rates of

Germany, the US and Japan."

This is in contrast to the supply side of the picture which was,

according to Natixis, surprisingly good in 2013 – mined output rose

around 8% during the year as new mines such as Oyu Tolgoi and Ministro

Hales came online and production from Collahuasi and Escondida surprised

on the upside – and likely to get better in 2014.

But, while mined output rose over the year, a variety of smelting

issues meant that refined copper was harder to come by, which explains

the rise in both treatment and refining charges and physical premiums.

According to Natixis, the combination of both the imminent arrival of

as much as an extra million tonnes of mined output per year and the

tightness currently on display accounted for the moderate rise in prices

to around $7,200/tonne.

But, it says, “Through the course of 2014, additional smelting (and

SX/EW) capacity should come on-stream, helping to facilitate a rise in

refined copper production and taking the market into a gradually

expanding surplus. This should ultimately limit gains in copper prices,

although the tightness of the market could push spot prices higher in

the very near term."

Wood Mackenzie believes that this surplus should last until around

2017, reflecting the various new projects that are coming online....MORE

2013 was a funny year

for blockbuster real estate—despite the fact that last 12 months were

seemingly packed with vanity pricing, nine-figure listings, and enough "historic" pedigrees,$20M-plus renovations, and beach frontage to give even die-hard consumers of ostentatious real estate a stomach ache, the crème de la crème of pricy listings have (surprise!) struggled to maintain their inflated asks, particularly when one looks at the fates of 2012's most expensive properties. Casa Casuarina, which was listed last year for $125M? Sold at auction for $41.5M. The three $95MNYCapartments? Yeah, not one sold. But what of the fates of this year's blockbusters? Well, Copper Beech Farm, which roared onto the market for an eye-popping $190M, has already been slashed by $50M.

The map below charts the 12 priciest properties to officially hit the

market in the Untied States in 2013, and the fates that have befallen

them. Do have a look:

Copper Beech Farm, the 50-acre (debt-laden) Greenwich estate that roared onto the market in May with a record-setting $190M price tag, has since suffered the fate shared by so many of its nine-figure peers: it's been mercilessly slashed, now asking$140M. Owned by timber mogul John Rudey, the property is stocked with a 12-bedroom mansion, a whopping 4,000 feet of water frontage, and not one, but two offshore islands. [link] Website

Crespi Estate, $135M

5555 Walnut Hill Lane, Dallas, TX 75229

In January, Texas business honcho Tom Hicks put his vast, Dallas, Texas, spread on the market for a staggering—nay, otherworldly—$135M, making it the priciest ask in the country at the time (no small feat, indeed). Despite once owning the Texas Rangers and being appraised by Forbes

in 2009 to have a net worth of about $1B, Hicks has stumbled

financially in the last few years, so it may be no real surprise that

he's looking to unload a house that is, as the Real Estalker points out, 10 times the size of the average American home. [link]

Dilbert's creator, Scott Adams must be wallowing in his outbreak of credibility or something; in years past Dogbert would have made sure he had the client's correct billing address.

It's all about the money (loot, swag, moolah, wampum, see blog descriptor above, etc) for the avaricious pooch:

Today's stroll down memory lane is prompted by this story at ABC News:

These days, everything is moving faster in the U.S., except for population growth.

According to the U.S. Census Bureau figures

released Monday, growth from July 1, 2012 through July 1, 2013 was 2.3

million people, or 0.71 percent of the total U.S. population.

That’s less than last year’s 0.75 percent growth, and the slowest rate since 1937.

Census Bureau researchers say the slow expansion of people in the

country is due to Baby Boomers, by far the largest segment of the

population, getting older, as well as fewer immigrants entering the U.S.

Meanwhile, in case you’re interested, the U.S. population when the

clock hits midnight Tuesday will stand at 317,297,938, give or take a

few people. That’s an increase of 2,218,622 from last New Year’s Day.

Political Calculations is quirky. On the one hand they link to Prof.

Shiller's merged Cowles/S&P data (first rate scholarship/database).

On the other they do a "On the Moneyed Midways" linkfest that seems

aimed at a totally different target audience. Here's an example of the

former:

There are two questions that we'll seek to answer in this post:

How might the change in a nation's population over time affect its rate of inflation?

Are U.S. baby boomers the most inherently evil generation ever in economic history?

Before we go any further though, for the sake of eliminating the suspense involved, here are the answers to both questions:

Predictably.

Yes.

We

are being a bit facetious with our second question, but let's see if

you don't draw a similar conclusion after we work through the first

question.

That question arises as we've recently been looking

to develop a model for anticipating the future rate of inflation in the

United States, which we could then incorporate into the kind of tools we

develop and make available to everybody in the world here at Political

Calculations. In doing that, we began with a July 2006 paper by Ivan Kitov, a geophysicist whose work in economics we first became familiar with back in 2005 (via one of David Smith's discussion forums, whose archives unfortunately appear to only go back four years), which has intrigued us for some time: Exact Prediction of Inflation in the USA.

In

the paper, Kitov presents his findings of a remarkable correlation

between the measured rate of inflation observed in the U.S. and the

change of the size of the U.S. workforce over the years from 1965

through 2002, which is observable in the figure we've excerpted from the

paper. In this chart, we see that inflation, as measured by the GDP

deflator, closely follows the trajectory determined by the change in the

size of the U.S. labor force (dLF) with respect to the total labor

force (LF) some two years earlier. In simpler terms, changes in the rate

of inflation in the U.S lag the change in the relative size of the U.S.

labor force by a two year period.

How That Might Work How

might changes in the size of the US. workforce drive changes in the

U.S. inflation rate? We suspect that the answer to that question lies in

the change in consumption patterns driven by those entering and exiting

the U.S. labor force....MORE, including some interesting charts.

I know it's getting repetitive but, "we're still looking for $875 sometime in Q3 2014".

Gold $1185.90 last, $1181.40 low.

Silver $18.87 last, $18.72 low.

From ZeroHedge:

As the US session starts, despite a dearth of news and actvity in

other markets, the precious metals complex is being smashed lower (on

heavy volume). Gold just hit 2013 lows at $1182 and Silver at $18.837 is near its 2013 lows also.

It seems someone wants the status-quo-defying precious metals going

out at their lows as central-planning-supporting stocks go out at their

highs...

You haven't seen much on equities on the blog for months. We've had the short then long Tesla trades which got close to the $160 target-$158.00- on the 26th and the hatin'-on-the-gold-miners shorts but for the overall market not many posts.

There are two reasons for the lack of commentary:

First, and overriding, I'm not that good in the latter stages of a bull market. Early on seems easy, catching the turn the day after the Mar. 9, 2009 bottom,* albeit thinking it was only the start of a six or so week rally, the confidence intervals were a lot higher then than they are as we approach the five-year anniversary in a few months.

As a side note the first part of the '80's-'90's Big Bull Market lasted 5 years and 13 days-from 776.92 on Aug. 12, 1982 to 2722 on Aug. 25, 1987.

The second reason for the lack of commentary has been the monetary environment-"Don't fight the Fed" on steroids.

As long as the federales are doing the QE thing the appropriate posture is to shade ones positioning to the long side while at the same time realizing it's a game of musical chairs where the one certainty is the music will stop, if for no other reason than to give the band a chance to grab a cocktail and change conductors, and since the underlying philosophy of the stuff we put out in public is higher certainty trades even if that means lower expected returns (you won't see many exotic or hybrid instruments, for example), when the certainty levels decline the appropriate action is to shut up.

In just the last ten days we're starting to see forecasts for 2014 which definitely carry a whiff of complacency with them, how the new year is shaping up to be the perfect economic environment for equities etc and that gets the antennae twitching.

Just so any future archeologists can ascertain whether we are even close to having a clue as to what is going on we try to include the level of the instrument on any post that might be construed as a recommendation, in this case it is the S&P 500 which looks to open at 1838 up 3.00 (or alternatively the DJIA which looks set to open at 16,472 up 33.00).

Finally, we don't have a lot of faith in Elliot Wave Theory, the "alternate" wave counts are just too loosey-goosey for holding the analyst accountable.

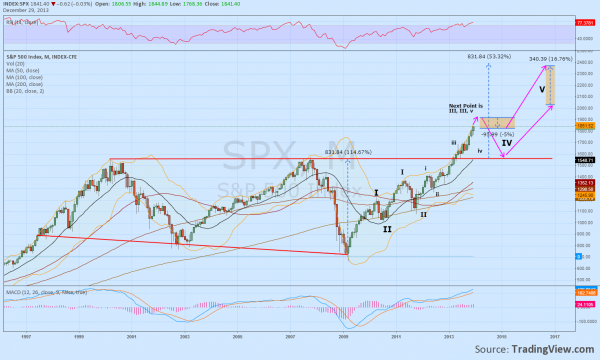

From Dragonfly Capital:

A year end series taking a longer perspective in many market

indexes, macro related commodities, currency and bonds. Over three

weeks these reviews are intended to help create a high level road map

for the the next twelve months and beyond. We finish today with the

S&P 500 ($SPY, $SPX).

The S&P 500 has long ago replaced the Dow Jones Industrial

Average as the benchmark index for most managers. And for good reason,

its broad constituency gives it enough diversification among the large

cap names to give a clear understanding of market direction. 2013 was a

breakout year for this index, breaking a 15 year channel of price

action and continuing the move higher since the bottom of the financial

crisis. It has climbed a wall of worry the whole way and there is still

a very low participation rate among individual investors. The monthly

chart below shows that channel and projects a target of 2400 on the

break out above it on a Measured Move. Another 550 points to go. Wow!

This can be roughly confirmed by using Elliott Wave principles as well.

Since the 2010 bottom the price action has been in Wave III

of the impulse higher. This is often the strongest wave. The fractal

nature of Elliott Wave shows this is also Wave III since October 2011

and Wave v within that Wave III. All that means is that it could make

an interim top shortly at 1923. That would be supported by the Relative

Strength Index (RSI), currently technically overbought, reverting

lower. The next wave, Wave IV, would be expected to be very flat as it

usually is opposite in nature to Wave II, which was down. Using a 5%

correction would bring it back to about 1820 before the Wave V higher to complete the bigger Wave III.

All this says that 2400 can be seen from 2 different perspectives.

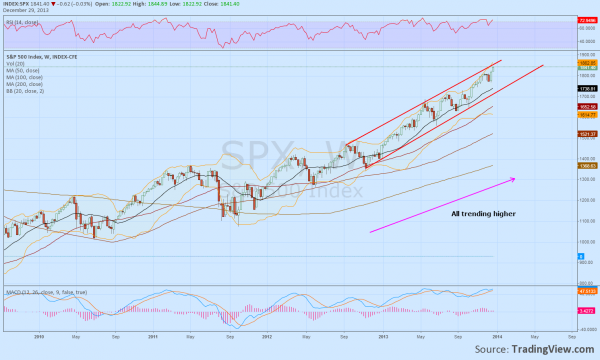

The weekly picture can help fill in some of the details along the way,

and I promise no more Elliott Wave. The chart below shows that the

S&P 500 has been in a rising channel, narrowing very slightly, since

the November 2012 launching point. Currently it is at the top of that

channel and with a RSI that is hovering around the technically

overbought level at 70 it would make sense if it reverted to towards the

bottom of the channel. The 20 week Simple Moving Average (SMA), also

roughly the 100 day SMA, has acted as support and is just above the

channel bottom. That would be a target entry point on a hold there if

it does pullback. All of the SMA are rising and have

good separation, as they move higher in a parallel fashion with the

price channel. This is a strong trend. The daily chart though suggests

that it may not get that low in the near term. The S&P broke a

rising wedge from July in October, retested it and has moved higher.

The recent break out of the yellow box has a Measured Move to 1848,

about where it is now, and near the round number 1850...MORE

It looks like more up, then down. Do click through for the larger charts.

Using the low I.Q. approach* to investment analysis, refined by yours

truly, while we will have some down days in the next two weeks, the

trend will be up. Then come the first quarter earnings reports and the crystal ball gets a bit cloudier....

Being on the right side of the move makes it easier to stay on the right side of the move.

Plus, it's pretty funny when the computers start asking if they can use some margin.

....A couple characteristics of big bull markets:

1) Once the move is underway waiting for a pullback almost guarantees

you will be underinvested. Everybody is waiting for a pullback, not

everybody has the fearlessness/foolishness to committ.

2) The market will find a way to make your day-to-day prognostications and pronouncements look stupid. Ease in, even if you have to grit your teeth and shut your eyes.

From ComputerWorld: The first 3D printed organ -- a liver -- is expected in 2014

Approximately 18 people die every day waiting

for an organ transplant. But that may change someday sooner than you

think -- thanks to 3D printing.

Advances in the 3D printing of human tissue have moved fast enough

that San Diego-based bio-printing company Organovo now expects to unveil

the world's first printed organ -- a human liver -- next year.

Like other forms of 3D printing, bio-printing lays down layer after

layer of material -- in this case, live cells -- to form a solid

physical entity -- in this case, human tissue. The major stumbling block

in creating tissue continues to be manufacturing the vascular system

needed to provide it with life-sustaining oxygen and nutrients.

Living cells may literally die before the tissue gets off the printer table.

Organovo, however, said it has overcome that vascular issue to a

degree. "We have achieved thicknesses of greater than 500 microns, and

have maintained liver tissue in a fully functional state with native

phenotypic behavior for at least 40 days," said Mike Renard, Organovo's

executive vice president of commercial operations.

A micron is one-millionth of a meter. To better understand the scale

Renard is describing, think of it this way: A sheet of printer paper is

100 microns thick. So the tissue Organovo has printed is the thickness

of five sheets of paper stacked on top of each other.

Liver tissue printed in a petri dish. (Image: Organovo)

Printing hepatocytes -- the cells that make up most liver tissue --

isn't enough, however. There are multiple types of cells with different

functions in tissue that must be combined to create a living human

organ....MORE

Stanford professor Andrew Ng teaching his course on Machine Learning (in a video from 2008)

“New Brainlike Computers, Learning From Experience,” reads a headline on the front page of The New York Times

this morning. The article focuses on machine-learning algorithms, known

as a neural networks, that are becoming increasingly important in

computer science. And in 2014 Qualcomm will release the first commercial

version of a neuromorphic processor that transforms this software

technique directly into hardware to increase performance for intensive

machine learning tasks.

But buried in the last paragraph of the story was the fact that “The

largest class on campus this fall at Stanford was a graduate level

machine-learning course covering both statistical and biological

approaches, taught by the computer scientist Andrew Ng. More than 760

students enrolled.” And several previous versions of the course are

available online for free. The most recent is from Coursera (which Ng cofounded with Daphne Koller last year) but the 2008 course is on iTune U, YouTube and Stanford’s Engineering Everywhere.

What’s going on here? Simply put, machine learning is the part of

artificial intelligence that actually works. You can use it to train

computers to do things that are impossible to program in advance. Ng

uses the example of handwriting recognition as a classic example of a

problem that can only be achieved through machine learning. In his introductory lecture

on Coursera, Ng refers to search engines like Google and Bing, Facebook

and Apple’s photo tagging application and Gmail’s spam filtering as

everyday examples of machine learning at work. Ng is the director of the

Stanford Artificial Intelligence Lab

and one of the founders, with Jeff Dean, of Google Brain, a deep

learning research project at Google. He is using machine learning as a

step towards the “AI dream of someday building machines as intelligent

as you or I.”...MORE

If only J.K. Rowling had written about metamaterials and perfect lenses.

John Pendry

is a physicist at Imperial College London who laid the theoretical

foundations for the invisibility cloak and superlenses capable of

producing the sharpest ever images. He talks about the profound physics

obscured by his invisibility cloak and how metamaterials could help

realize the perfect lens.

Valerie Jamieson: Invisibility cloaks can guide light around

objects as if they weren't there. It is awe-inspiring physics. So why

the frustration? John Pendry: It's when I give talks, particularly popular ones. Of all the things I am interested in, I am always asked about invisibility cloaks.

I think, "Oh God, not another invisibility cloak lecture." I still

enjoy giving them, but there are many other things I'm working on that

are more profound; they just don't have that fertile soil which J. K.

Rowling prepared for us.

VJ: What topics do you wish were better-known? JP: The concept of a perfect lens

is profound. A lens is a complicated thing that takes every point in an

object and reconstructs it in the image—with no loss of detail in the

case of a perfect lens.

VJ: An ordinary microscope or telescope can't see detail on a

scale less than the wavelength of light. You realized it was possible

to break this diffraction limit. How? JP: I knew that Russian engineer Victor Veselago had

theorized a lens made out of material with a negative refractive index.

In 1999 I checked whether such a lens could be perfect, expecting the

usual answer—that it wasn't perfect. I didn't get it; the theory said it

was perfect. I was astonished, and so was everybody else. The mechanism

of a perfect lens is very strange. I still get letters saying that it

is all rubbish, but this has died down.

VJ: How did the perfect lens go from theoretical possibility to reality? JP: The concept of metamaterials

opened up the field. A metamaterial is a material whose electric and

magnetic properties are determined as much by its structure as by its

chemical composition, although the structure must be on a scale much

smaller than the wavelength of light you're using. The real kick-start

came when I got together with a team in San Diego who made the first

material that had a negative refractive index, which was something of a

Holy Grail for electromagnetism. It had been talked about for many, many

years but you just couldn't find any stuff that did that.

VJ: Experimentally, what has been achieved? JP: A perfect lens is very hard to realize in the lab.

People have achieved sub-wavelength resolution that is more than 10

times as good as a normal lens, but it is far from being used as a

microscope.

VJ: Can these lenses be used for anything else? JP: There is a halfway house that my research team

in London is working on—a light harvester. It concentrates light on a

very small area. Ordinarily the area you can shrink to will be limited

by the wavelength of the light you are using, as an ordinary lens is. We

are using metamaterials to concentrate light onto an area less than a

square nanometer. Once you do that, you have the potential to make

sensors for single molecules.

VJ: Will metamaterials win a Nobel Prize? JP: All I can say is that I hope they will. It is a lottery, isn't it really?

VJ: If you met J. K. Rowling, what would you say? JP: I'd be in awe. I'd let her speak first, like the Queen.

Just about the time 'the 'stans' start receding from the Western headlines it is probably most important to think about them.

From ZeroHedge:

Submitted by Paul Mylchreest of Monument Securities

Sir Halford Mackinder’s 1904 speach in which he outlined his

“Heartland Theory” was a founding moment for geo-politics. He argued

that control of the Eurasian landmass (Europe, Asia and the Middle

East), which contained the bulk of the world’s population and natural

resources, was the major geo-political prize.

As time passed, energy (first crude oil then natural gas), became

increasingly integral to this concept and its strategic significance

cannot be overstated.

Remarkably, Mackinder’s theory has remained equally valid, if not

more so, in the modern era - although key “pivot areas” for exercising

control have evolved. In addition to Central Asia and Trans-Caucasus in

Mackinder’s day, the oil producing nations of the Middle East took on

increasing importance in the “New Great Game”.

The geo-political confrontation between the US on one hand and China

(in increasingly close cooperation with Russia) on the other, is

evolving rapidly. We see a “New New Great Game” (NNGG) emerging and have

“tweaked” the Heartland Theory to include....

....The “New New Great Game” Mackinder’s “Heartland Theory”

The traditional “Great Game” obviously dates back to the

geo-political rivalry between Great Britain and Russia for supremacy in

the central Asian region during the nineteenth and early part of the

last century. In his famous speech, “The Geographical Pivot of History”,

to the Royal Geographical Society in 1904, Sir Halford Mackinder

outlined his “Heartland Theory. ” According to Wikipedia.

“This is often considered a, if not the, founding moment of geo-politics...”

Briefly, this posited that the major geo-political prize is Eurasia

(the “World Island”), i.e. the European, Asian and Middle Eastern land

mass, which contained the bulk of the world’s population and its natural

resources. Mackinder argued that control of the “pivot area“ of central

Asia was the key to controlling Eurasia.

This is taken from his paper published in the April 1904 edition of the “The Geographical Journal.”

He also emphasised the important difference between sea power and

land power. From Zurich-based ISN’s 2009 “Geopolitics and US Middle

Eastern Policy: Mackinder and Brzezinski.”

“Mackinder’s theory was a counter-argument to notions that maritime

supremacy was sufficient for a power such as Great Britain to safeguard

its hegemony. He claimed that, with the emergence of new transportation

routes [e.g. Trans-Siberian railway] and technology, a power that could

control the centre (and the abundant resources) of the Eurasian

landmass...would ultimately be able to attack the colonies of a sea

power everywhere on the continent. “

The Trans-Siberian Railway.

In the wake of World War One, Mackinder argued the case for

preventing a convergence of interests between Russia and new “pivot”

states of Eastern Europe (Austria, Hungary, Czechoslovakia and Poland).

This led to his famous dictum. “Who rules East Europe commands the Heartland; Who rules the Heartland commands the World Island; Who rules the World Island commands the World.”

It’s important to emphasise that the pivot area does evolve/fluctuate

with changes in geo-political reality. Indeed, Mackinder included the

Baltic states in one of his revisions.

As the world industrialised and became increasingly dependent on

crude oil (and later, natural gas), energy resources became ever more

integral to the Great Game. With such a large proportion of the world’s

oil and gas reserves found on the Eurasian land mass, this was easily

accommodated within Mackinder’s theory.

The period just before World War One, with the British Navy’s switch

from coal to oil and the adoption of the automobile, set the stage for

this. Indeed, in 1913, the British government acquired a 51% controlling

interest in the Anglo-Persian Oil Company, the forerunner of BP.

Remarkably, the validity of Mackinder’s theory has stood the test of

time, even though most people are unfamiliar with it. The following

quote is from the Reagan Administration’s “National Security Strategy of

the United States” published in January 1988.

“The first historical dimension of our strategy is

relatively simple, clear-cut, and immensely sensible. It is the

conviction that the United States’ most basic national security

interests would be endangered if a hostile state or group of states were

to dominate the Eurasian land mass – that area of the globe often

referred to as the world’s heartland.”

Right now, it’s obvious that US national security interests are threatened by a combination of China and Russia.

This was the influential globalist (and former National Security

Advisor), Zbigniew Brzezinski, writing in his famous 1997 book, “The

Grand Chessboard.”

“Ever since the continents started interacting

politically some 500 years ago, Eurasia has been the centre of world

power… For America, the chief geopolitical prize is Eurasia – and

America’s global primacy is directly dependent on how long and how

effectively its preponderance on the Eurasian continent is sustained.”

In the “New Great Game”, (NGG) of the modern era, the major rivalry

is between US/NATO on one side and China, Russia, other members of the

Shanghai Cooperation Organisation and the likes of Iran, on the other.

The “pivot states” in the NGG are.

The key nations in Central Asia and the Trans-Caucasus: especially

those with substantial energy resources and/or pipelines (e.g.

Azerbaijan, Ukraine, Turkmenistan, Uzbekistan etc). Here is a chart

showing the major gas pipelines

We looked at Rap Genius in 2012's "Why Andreessen Horowitz Is Investing in Rap Genius".

In a nutshell the company intended to expand from explanations of rap lyrics to explanations of the entire universe (or something).

Here's the headline story from The Daily Dot: The real problem with the fall of Rap Genius

You may have already heard what happened to Rap Genius

last week. A Web developer caught the lyrics analysis site in an

elaborate scheme to ensure that links to its pages topped the Google

results for rap and pop lyrics searches. To penalize the site for its

shady dealings, Google knocked it far down in the rankings, even in

searches for "rap genius."

Rap Genius responded

with the sort of Janus-faced apology that's been standard operating

procedure on the Internet in 2013: Yes, we did something wrong, but most

of our competitors are doing it, too. The apologetic half would sound

far more genuine were it not paired with a rationalization. The

rationalization would make for a pretty reasonable point had it come

from just about anyone else.

With news sites splitting their time between enjoying Rap Genius' comeuppance and speculating on whether the move will kill them outright,

an aspect of the story that's taken largely for granted is Google's

Zeus-like power to strike an offending site with lightning.

That isn’t to say that Rap Genius was in the right, or that Google

abused its power in taking the site down a few notches. If a site wants

the benefits of search visibility, it should be prepared to play by the

rules of search providers. If search providers want sites to obey their

rules, they have to be prepared to penalize those that don't. Rather,

the problem is with the online market, and the way in which we've

allowed a few powerful services to grow into gatekeepers for the rest of

the Internet.

To understand why that’s the case, it’s important to acknowledge that

one of the more enduring difficulties created by digital media is the

way in which it conceals. That leads to a number of problems variously

termed “visibility” or “discoverability,” but which can be illustrated

by imagining that you’re in the waiting room of a doctor’s office,

looking for something to read. Because print magazines are physical

objects, each one asserts its own presence simply by virtue of the space

it occupies. One may get buried under the others, or slip behind a

chair, but it should be easy to sort through them to find one that

interests you.

What happens, though, when you copy those magazines into the virtual

space of a tablet or smartphone? Since they no longer take up a

discernible physical space, there’s no obvious way to sort through

them—unless, that is, someone builds one. Without the reader app on your

device, it would be significantly more difficult to find the magazine

you want; without some basic menu functions, you’d be unable to access

them at all.

Most of the interfaces we deal with on digital platforms are just that:

solutions for sorting information in a way that makes the concealed

accessible to humans. Menus work well enough when you’re dealing with a

dozen magazines or so, but when you’re dealing with millions of pages,

you need a more powerful way to sort and index all that information.

That’s where search engines step in. They’ve long since proven

themselves as an effective way of navigating the wealth of sites and

pages on an ever-growing network, but they’ve bred a reliance from which

even the sharing economy of social media has failed to wean us. To an

unsettling degree, we’re dependent on search, and more and more over the

last 25 years, that’s meant a dependence on a single search provider.

Before Google achieved dominance, there were dozens of options—like

Lycos, Infoseek, and the recently departed Altavista—each delivering a

slightly different view of the Web. Some of the early contenders are

still around, but none comes close to the market share held by Google.

In 2013, it handled slightly more than two-thirds

of the searches conducted on the Web. Even sharing search results

between them, Yahoo and Microsoft’s Bing only managed about 11 percent

and 17 percent respectively, with everyone else netting single-digits or

a fraction of a percent.

Google’s gotten there by maintaining a nimble and reliable search

algorithm, which might make this seem like an example of fair

competition producing a clear winner. That’s an immense amount of power

to concentrate in a single company, though, and it has consequences for

how the Web as a whole operates....MUCH MORE

From the Washington Post's The Insiders' Game special report:

I’d been at the Post only a few months in 1988 when the managing

editor, Robert Kaiser, walked into my office, closed the door and tossed

onto my desk the section from that day’s paper containing the list of

recent home sales in the District. One sale was circled — mine.

Bob’s message that afternoon was that I’d broken an unwritten

rule by buying an $830,000 house in an upscale neighborhood of Northwest

Washington. Post journalists were not supposed to call attention to

themselves in that way, he explained. I had chosen a house that didn’t

reflect my proper place, as a mid-level editor, in the pecking order of

Washington. Because I was new in town, he wanted to warn me about my

violation of this unwritten code.

The son of a diplomat and academic, Bob grew up in a Washington

where your place in the social order wasn’t determined by how much money

you had but by how much power and influence you had and how much

respect you commanded. It was all about what you did and what you knew,

not what you had.

Even the few who had wealth abided by the old-money ethic that

you didn’t flaunt it — and most certainly you didn’t talk about it.

Washington back then thought of itself as a city that existed for one

purpose, to serve the public.

If that strikes you today as incredibly hokey and naïve, consider

it a measure of how much the culture of Washington has changed in the

past 30 years. In almost every way, the region continues to be shaped by

the presence of the federal government. But as this series, the

Insiders’ Game, has richly illustrated, the idea of “serving the public”

has taken on a somewhat different meaning — one less rooted in

sacrifice, stewardship and the chance to make a difference, one more

given to celebrity, manipulation and the chance to make a big score.

This transformation was not part of some grand strategy hatched

over lunch at the Metropolitan Club to make this the richest region in

the country. Nor was it some mysterious breakdown in the moral fiber of

those living in the capital. According to those who lived through it,

the explanation is a whole lot more simple: The nation changed and

Washington changed with it.

(Andre da Loba/For The Washington Post)

Still small and Southern

In the decades after World War II, Washington was something of a

middle-class paradise, a company town where a rapidly growing government

provided reliable jobs and steady income to a wide range of Americans

who flocked here — black and white, urban and suburban, high skilled and

low, ambitious and risk-averse....MUCH MORE

This is almost a year old but I wanted it on the blog as a reference.

I haven't seen anyone post a 120-125-year study of the fraction of corporate profitability used to pay wages and salaries; fringe benefits such as corporate pension contributions, health care, vacation time etc; corporate taxes; plant, property and equipment; dividends-pretty much the whole schmear.

I'll probably have to commission something to get what I want but here's a start.

Some of the dates to watch for: The 1870's for the rise of the trades/crafts/labor unions;1913 when the 16th amendment passed, marking the start of income taxation; the use of medical coverage as an inducement to employees under WWII's wage and price controls; the big shift during the 1980's from defined benefit to defined contribution retirement plans and a few others that readers know better than I.

From the PBS NewsHour's Business Desk:

Today we welcome once again our friend and monetary minstrel Jon

Shayne, aka Merle Hazard, a Nashville investment manager. Shayne has

written and sung such classics as "H-E-D-G-E," "In the Hamptons," "The

Greek Debt Crisis" and "Inflation or Deflation?" He shared one of his

latest hits, "Fiscal Cliff," with us on Making Sense. You can access his entire oeuvre here.

Today, he conducts an interview with Andrew Smithers, a British economist. We'll let him take it from here.

Jon Shayne: Late last year, Andrew Smithers answered questions

on this page about how labor's share of output in the U.S. has declined

over the past thirty years. Judging from the comments received and

other reader reaction, many of you would like to hear more about the

topic. Andrew was kind enough to agree to answer another round of

questions.

This graph of his, which we also used in the first interview, shows how much labor's share has declined, in favor of capital's:

U.S. Department of Commerce, Bureau of Economic Analysis.

Andrew formerly ran the asset management business of S.G. Warburg,

and now heads up his own consulting firm, Smithers & Co., in London.

In our last interview, he explained his view that the movement toward a

"bonus culture," in which business managers get paid for short-term

rather than long-term profits, is responsible for the diminishment in

output going to labor.

Jon Shayne: Andrew, a reader asked whether the

problem of labor's lower share can be solved by higher income tax rates,

at least on those with very high incomes. Can it? Andrew Smithers: Yes, it would, I think, fix the

problem, but it would probably cause a great deal of other damage -- for

example many of the best U.S. managers and entrepreneurs might choose

to emigrate, as French ones are doing in response to high threatened

French taxes. We need a solution to the perverse incentives of the

modern bonus system, but a better one than very high marginal tax rates.

Jon Shayne: In our prior piece, you said that the

respective shares of labor and capital are mean-reverting. In other

words, you are saying that labor's share will, in time, go back up to

its average level, and capital's share will go down. Why? Is the

mechanism of reversion political, or more purely economic? Andrew Smithers: It's economic. Companies can

increase output either by using more capital, more labor, or both. They

will choose what's best for them. Adding more labor without adding more

capital, or adding more capital without adding more labor, will be less

efficient than adding both. With this simple assumption economists have

shown that profit margins are in theory mean-reverting.

This is one of those all-too-rare economic theories which is

supported by the evidence. Professor James Mitchell, of the University

of Warwick, has done a statistical analysis of the US data from

1929-2011 that confirms the US profit margins are mean-reverting. I will

put be putting some of the details of his research into the appendix of

an upcoming book of mine.

Note from JS: In the background of Andrew's answer is the idea

that as technology, i.e. capital, improves, it produces more output per

hour of labor. This actually makes workers more valuable to employers.

All else equal, employers then bid up the price of labor. This is an

economic explanation of why living standards have risen over time. Jon Shayne: Paul Krugman has raised the possibility

that labor's current lower share could be a result of technological

advances or looser antitrust enforcement. Or a combination of the two.

You gave evidence in the prior interview that technology is not the real

issue here, but what do you think about looser antitrust enforcement,

which seems to have begun during Ronald Reagan's presidency, as an

explanation? All else equal, if a business gains some degree of monopoly

power, it can make prices and profits go up, without raising wages. Andrew Smithers: The argument for increased monopoly

power is, next to the perverse impact of the bonus culture, the best

available explanation that I have seen of the level of profit margins

and cash flow surpluses of the business sector in the UK and U.S. In

fact the two explanations have much in common.

Companies have a great deal of monopoly power in the short term.

Unless spare capacity is massive, buyers cannot shift easily to new

sources of supply. Managements are thus always making judgments when

they make pricing decisions. The risk they take in keeping up margins is

that they will increasingly lose market share over time. The risk they

take if they allow margins to narrow is that they will make lower

profits in the short term. They have to judge between similar risks when

taking decisions on investment. The long-term risk of not investing is

that they will have higher production costs than their competitors over

time, and the risk of investing is that it will lower profits and, in

addition, profits per share. (In the latter case because money spent on

new investment cannot be used to buy back shares.)

The bonus system encourages management to play down the longer-term

risks in order to maximize short term profits per share. It is in effect

an encouragement to exploit short-term monopoly power more aggressively

than before.

The effect of the bonus system and a rise in monopoly power are thus

very similar in many ways. In both cases, profit margins will rise and

investment will not rise proportionately, as the rise in monopoly will

probably affect the return on existing capital rather than new.

There are, however, some points which make the bonus culture the better of the two explanations.

1) The evidence for an increase in monopoly power is, as far as I

am aware, limited to the evidence that profit margins are unusually high

and business cash flow unusually strong. But the evidence for the

change in business incentives is independent. We don't therefore need to

assume that monopoly power has changed and the principle of parsimony

(Ockham's razor) suggests that the bonus culture should be the preferred

explanation unless other evidence for rising monopoly is produced for

both UK and the U.S.

2)The bonus culture encourages companies to report highly volatile

profits, but this does not apply to an increase in monopoly. US reported

profits have become much more volatile than the profits shown in the

NIPA, as I show in the Chart below. (NIPA is the National Income

Products Account series, published by a division of the US Dept. of

Commerce.)

Note from JS: Even if domestic competition has lessened, it is also

possible, or likely, that international competition has intensified.EPS is Earnings per Share

Jon Shayne: You disagree, then, with the

conventional wisdom, at least the old conventional wisdom, that public

companies use accounting techniques, some might say tricks, to smooth

their earnings? Andrew Smithers: They may have smoothed earnings a

bit in the past. Up to 1990, the volatility of published profits was a

bit less than the volatility of NIPA profits, but management now wants

volatile earnings and, as the chart shows, what management wants,

management gits....MORE

As Political Capitalism

becomes indistinguishable from Mussolini's Corporatism it's getting

close to the time where the West has to decide just what it wants to be

when it grows up.

"The

rich and powerful too often bend the acts of government to their

selfish purposes, many of our rich men have not been content with equal

protection and equal benefits, but have besought us to make them richer

by acts of Congress." Andrew Jackson (1830) Cited by Charles Sellers, The Market Revolution: Jacksonian America 1815-1846.

New York: Oxford University Press, 1991, p. 62

"Capitalism's

biggest political enemies are not the firebrand trade unionists spewing

vitriol against the system but the executives in pin-striped suits

extolling the virtues of competitive markets with every breath while

attempting to extinguish them with every action." Raghuram Rajan and Luigi Zingales, Saving Capitalism from the Capitalists. New York: Crown Business, 2003, p. 276.

And yes, I know the distinction

between Fascism and vertical syndicalist corporatism based on guilds.

I'm just using a shorthand, readily understandable usage....

Phrases such as "...the distinction

between Fascism and vertical syndicalist corporatism based on guilds" make me the hit of any party.

From naked capitalism's Yves Smith writing at Truth-Out:

President

Barack Obama meets with technology company executives to discuss

surveillance and health care in the Roosevelt Room of the White House in

Washington, Dec. 17, 2013. From right: Obama; Marissa Mayer, the chief

executive of Yahoo!; and Mark Pincus, a co-founder of Zynga. (Gabriella

Demczuk/The New York Times)

I’m actually a bit miffed that Konczal treats the “corporatism”

appellation as the sole property of the right wing (in the style sheet

of the Vichy Left, calling them “hysterics” is redundant but necessary

for the rubes), since I have a prior claim. And what is particularly

rich is that Konczal apparently regards the allusion to Mussolini to be

unfair:

Right-wing critics have a new favorite word to malign President

Obama’s economic policies: corporatism. Naturally, it’s an ugly word.

Whether it evokes Benito Mussolini’s fascist Italy or just an image of

the rich growing richer through government collusion, it’s a vision

nobody would defend. Nobody is for corporatism.

“Nobody is for corporatism”? Huh? Why does

Konczal think K Street and “think tanks” which for the most part the

arms and legs of corporations, exist? There is an entire large, well

funded, and extremely effective business apparatus that extracts

lucrative programs, explicit subsidies, guarantees, and various other

gimmies from government bodies at all levels. Tom Ferguson has been

meticulously documenting since the early 1980s how campaign finance in

America works, which he calls he calls the “investment theory of politics“:

that political parties in the US respond not to popular will or the

interests of broader society, but the patronage of large money blocks,

with certain industries preferring one party to the other.

One suspects the reason for the sensitivity within the ranks of the

Democratic party water-carriers to the “corporatist” label is that

Obamacare is a textbook case. Konczal cleverly tries to undermine this

charge by serving up an example of histrionic right-wing messaging:

depicting the contraception requirement (PR-wise, the Republican have

been big on throwing identity politics into the ACA mix, but they are

hardly alone).

Yet Obamacare IS corporatist. Here we have the industries that are

significant contributors to why the American medical system is so

overpriced – the health insurers and Big Pharma – actually playing a

major role in writing the legislation. And how is it not a sop to large

companies to have the government require that citizens buy your product

or else pay large tax penalties? Mr. Market certainly thought so, for

the price of health insurer and drug company stocks jumped the day the

ACA passed. And remember, the beneficiaries of Obamacare extend beyond

the insurers and pharmaceutical makers. Hospitals, who increasingly

engage in oligopoly pricing (most surgeries need to be done in

hospitals), also come out even stronger because new requirements imposed on doctors’ practices

will make it difficult for a retiring MD who practices medicine, as

opposed to servicing the rich (e.g., cosmetic surgeons) to sell their

business to anyone other than a hospital.

And the label fits in the banking arena like a glove. I’ve been

called both the Bush, but far more often the Obama bank-friendly

policies “Mussolini-style corporatism” since 2008, and well before what

Konczal claims is the origin of this description, Tim Carney’s book

Obamanomics, published November 30, 2009.

We used this expression September 28, 2008, in Mussolini-Style Corporatism in Action: Treasury Conference Call on Bailout Bill to Analysts.

And as much as the TARP was a Bush creation, remember that it was nixed

by Congress the first time it was presented. Obama, who was seen as the

likely next President, not only supported it, he whipped aggressively

for it. So TARP has the fingerprints of both parties all over it....MUCH MORE

The thing I learned from the Mike Konzcal piece at The New Republic

is how silly he looks trying to argue that "no, really, the emperor does

have clothes on".

Good grief.

"Fascism should more appropriately be called Corporatism because it is a merger of state and corporate power. "

-B. Mussolini via BrainyQuote

Here's a gentle poke at the Speaker.

Because at Climateer Investing we're nothing if not equal opportunity,

We'll be back with more on the new chairman of the President's Council on Jobs and Competitiveness.

His record at GE, the destruction of shareholder wealth, the shipping

jobs to China programs, the bailouts and guarantees, crony capitalism,

Mussolini style corporatism and power elites, the 3.6% tax rate,

subsidies and Davos, all in good fun, of course.

2013 was a funny year

for blockbuster real estate—despite the fact that last 12 months were

seemingly packed with vanity pricing, nine-figure listings, and enough "historic" pedigrees, $20M-plus renovations, and beach frontage to give even die-hard consumers of ostentatious real estate a stomach ache, the crème de la crème of pricy listings have (surprise!) struggled to maintain their inflated asks, particularly when one looks at the fates of 2012's most expensive properties. Casa Casuarina, which was listed last year for $125M? Sold at auction for $41.5M. The three $95M NYC apartments? Yeah, not one sold. But what of the fates of this year's blockbusters? Well, Copper Beech Farm, which roared onto the market for an eye-popping $190M, has already been slashed by $50M.

2013 was a funny year

for blockbuster real estate—despite the fact that last 12 months were

seemingly packed with vanity pricing, nine-figure listings, and enough "historic" pedigrees, $20M-plus renovations, and beach frontage to give even die-hard consumers of ostentatious real estate a stomach ache, the crème de la crème of pricy listings have (surprise!) struggled to maintain their inflated asks, particularly when one looks at the fates of 2012's most expensive properties. Casa Casuarina, which was listed last year for $125M? Sold at auction for $41.5M. The three $95M NYC apartments? Yeah, not one sold. But what of the fates of this year's blockbusters? Well, Copper Beech Farm, which roared onto the market for an eye-popping $190M, has already been slashed by $50M.

(Andre da Loba/For The Washington Post)

(Andre da Loba/For The Washington Post)

Note from JS: Even if domestic competition has lessened, it is also

possible, or likely, that international competition has intensified.

EPS is Earnings per Share

Note from JS: Even if domestic competition has lessened, it is also

possible, or likely, that international competition has intensified.

EPS is Earnings per Share